-

Industries

Healthcare & Compliance

Patient data systems, compliance reporting, and workflow automation for regulated environments.

- HIPAA-aware integration pipelines

- Automated compliance dashboards

- Patient workflow digitization

Logistics & Supply Chain

Real-time tracking, route optimization, and inventory visibility across your distribution network.

- ERP/WMS integration

- Automated dispatch workflows

- Supply chain dashboards

SaaS & Tech-enabled

Scale your product infrastructure, integrate third-party tools, and ship features faster with reliable ops.

- API-first architecture

- Multi-tenant infrastructure

- CI/CD and release pipelines

Banking & Financial

Secure transaction processing, regulatory reporting, and customer-facing portals for financial services.

- Regulatory reporting automation

- Secure data integration

- Customer portal modernization

- Case Studies

Featured Case Studies

Browse all case studies →Euro Truck ServiceLogistics firm automated 12 manual workflows in a single 30-day sprint

"Read case study →Ergonnex AI 360Ergonnex AI 360 is a powerful project management platform that helps IT companies manage their projects better with built-in AI-powered analytics

Read case study →PanoramikPanoramic caters to your passion for sharing photos in a social media environment.

Read case study →

Introduction

Financial institutions have continuously made efforts to deliver seamless banking experiences. However, with legacy systems, increasing compliance demands, and rising customer expectations, manual processes have become inefficient and unsustainable.

Today, automation is helping banks adapt to these pressures by transforming traditional operations into faster, smarter, and more modern systems. From large financial institutions to agile fintech startups, leaders are turning to automation to sustain growth and remain competitive.

However, financial services automation doesn’t work in isolation. Several key technologies are driving this shift. In this blog, we’ll explore the core technologies powering financial process automation—and how they’re making operations quicker, more accurate, and more responsive.

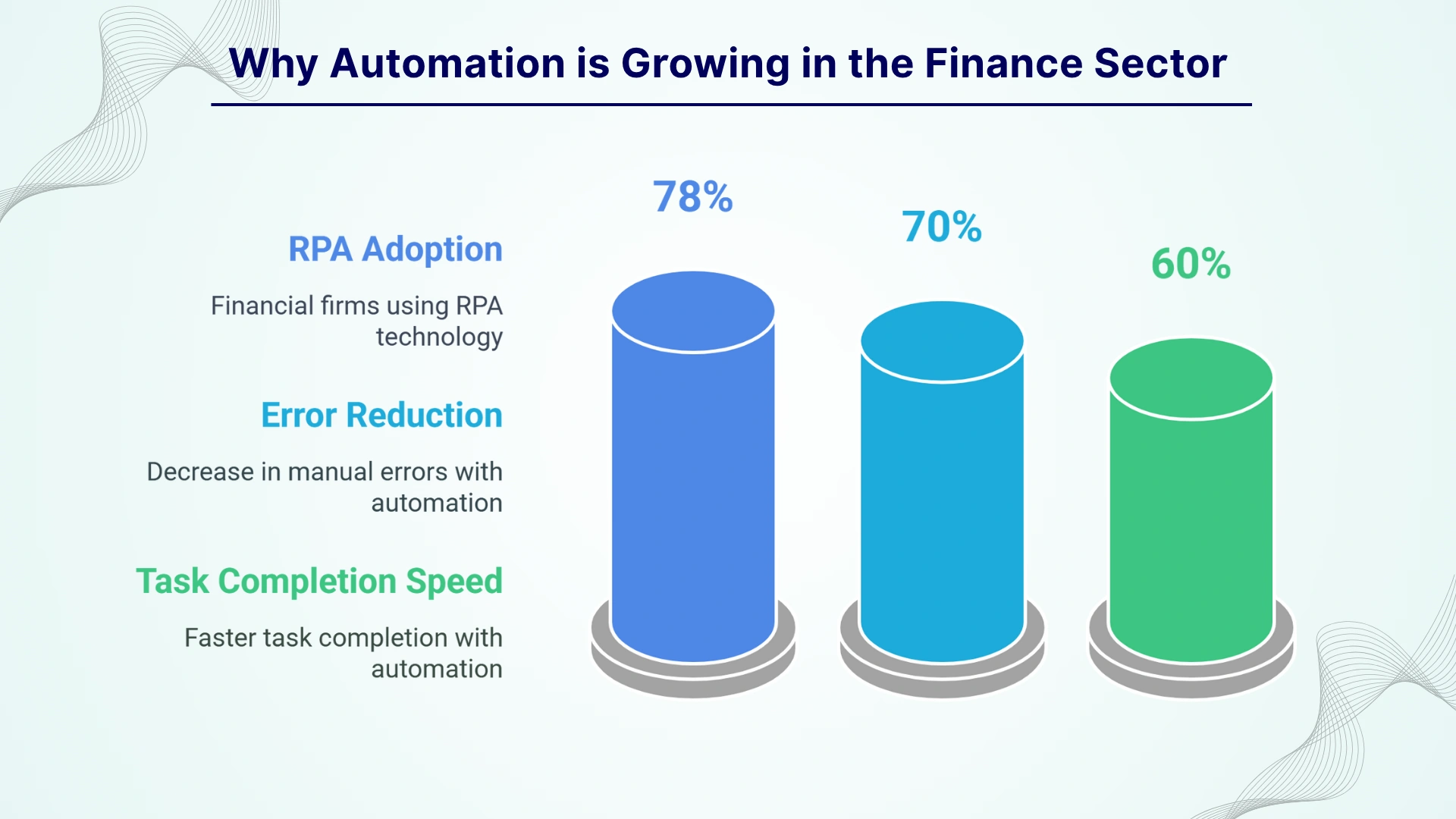

Why Automation is Growing in the Finance Sector

Automation is quickly growing among financial institutions all over the world. Technologies like RPA and AI are allowing banks to automate time-taking processes to optimize their completion from hours to minutes.

With its capabilities, Implementing financial services automation can enhance work efficiency, reduce costs, improve accuracy, and enable better decision-making. What started as a tool for reducing repetitive work is now turning into a key driver for transformation.

Here’s what market data says:

- Around 78% of financial firms have adopted RPA in at least one area.

- Automation tools have shown up to 70% fewer manual errors.

- Financial employees using automation complete tasks 60% faster, especially in areas like fraud checks and compliance reporting.

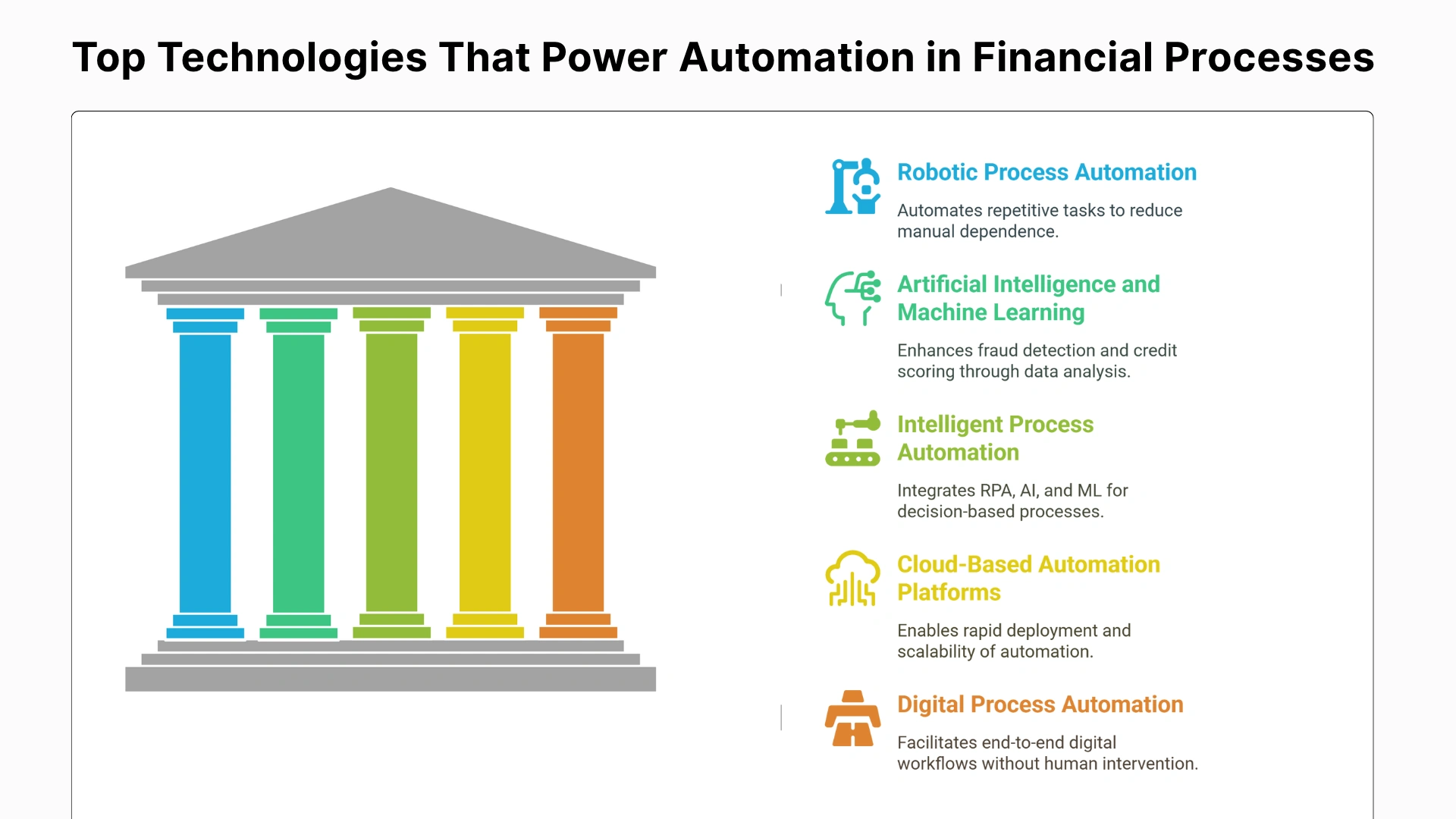

Top Technologies That Power Automation in Financial Processes

The automation of banking processes has evolved significantly. From rule based repetitive tasks to now intelligent data sensitive operations, the use of automation has expanded through integrations with powerful tools. Here are some advanced technologies driving finance automation solutions:

The automation of banking processes has evolved significantly. From rule based repetitive tasks to now intelligent data sensitive operations, the use of automation has expanded through integrations with powerful tools. Here are some advanced technologies driving finance automation solutions:

Robotic Process Automation (RPA)

RPA is the most common automation platform and is used for automating tasks that are high in volume, follow repetitive procedures, or are rule-based. Banks of all sizes leverage this tool to complete workflows and reduce manual dependence.

Benefits of Robotic Process Automation in Financial Operations

- Speeds up processes like KYC or account opening.

- Reduces human error in data entry and reconciliation tasks.

- Cuts operational costs by automating repetitive, time-consuming back-office functions.

Artificial Intelligence (AI) and Machine Learning (ML)

AI analyses large datasets to uncover patterns and insights, while ML continuously improves performance based on past data. These technologies are used for fraud detection, credit risk assessment, and portfolio management.

Transformative Benefits of AI and ML in Finance

- Improves fraud detection by identifying suspicious patterns and learning evolving tricks.

- Enhances credit scoring using dynamic data models.

- Enables smarter investment and portfolio recommendations.

Intelligent Process Automation (IPA)

IPA technology combines RPA, AI, ML, and advanced analytics into one cohesive automation layer. It helps banks in handling decision-based processes that often need human intervention, such as loan approvals or compliance checks.

Benefits of IPA in Financial Processes

- Automates complex decisions with greater accuracy and consistency.

- Improves customer onboarding with faster document and identity checks.

- Eases compliance reporting by auto-validating rule-based exceptions.

Cloud-Based Automation Platforms

Cloud platforms offer flexibility, scalability, and security for deploying automation tools across global operations. Banks using these platforms can adopt automation faster and integrate seamlessly with core banking systems.

Benefits of Cloud-Based Automation Platforms

- Enables rapid deployment of automation across multiple branches.

- Scales automation capacity during high transaction periods.

- Reduces infrastructure costs and enhances system uptime.

Digital Process Automation (DPA)

DPA is a component of Hyperautomation which focuses on enabling end-to-end digital workflows in banks. Rather than automating the single process, it removes the need for human involvement and handles the whole process independently and accurately.

Benefits of End-to-End Digital Workflows in Banks

- Handles full processes like loan origination without manual steps.

- Improves turnaround time across departments.

- Delivers consistent and accurate customer outcomes even at a larger scale.

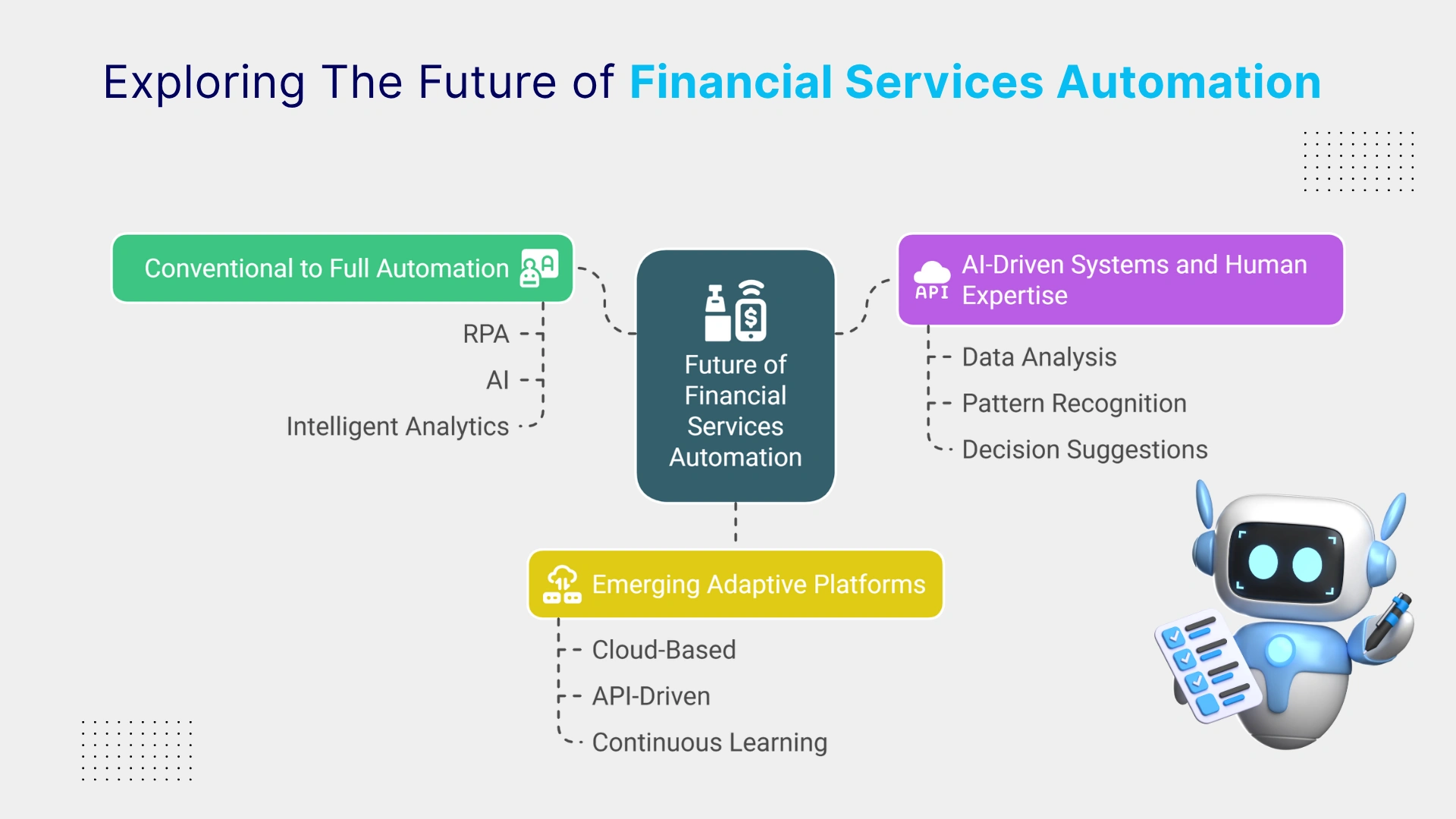

Exploring The Future of Financial Services Automation

Considering the demonstrated impact of automation in financial operations, future developments will focus on increasing accuracy, scalability, and integration efficiency. Here’s what to expect next:

Considering the demonstrated impact of automation in financial operations, future developments will focus on increasing accuracy, scalability, and integration efficiency. Here’s what to expect next:

1. Conventional automation to full automation: The isolated implementation of automation might not be as common in the coming years. Banks may shift significantly toward full lifecycle integration, where automation combines RPA, AI, and intelligent analytics to enable end-to-end finance automation.

2. Combining AI-driven systems and human expertise: Rather than replacing humans, future automation systems will work alongside them. AI will handle large-scale data analysis, pattern recognition, and decision suggestions, while finance professionals focus on complex judgment calls, ethical considerations, and strategic planning.

3. Emerging adaptive platforms: Next-gen automation platforms will be built to adapt. These cloud-based, API-driven systems will continuously learn from data, adjust to regulatory shifts and scale with business needs.

Do you have more questions?

Have a one on one discussion with our Expert Panel

Power Automate vs Logic Apps is one of the most common architectural decisions Microsoft shops face in 2026, and the stakes are higher than they look. Both tools automate workflows inside the Microsoft stack, both connect to hundreds of services, and both claim to solve

Every bank today is trying to do more with the same teams. Customer emails are increasing, compliance checks are getting stricter, and service expectations are becoming instant. Yet most internal processes still depend on manual steps. Employees move data from one screen to another, verify documents by hand, and follow long approval chains.

Many enterprise teams treat identity and access as if they are the same thing. They aren’t. Identity confirms who a user is. Access defines what that user is allowed to do. Assuming that an authenticated identity automatically deserves access is one of the most common—and costly organizational security mistakes.

Sahil Kataria

Founder and CEO

Amit Kumar

Chief Sales Officer

QServices Inc. undertakes every project with a high degree of professionalism. Their communication style is unmatched and they are always available to resolve issues or just discuss the project.