-

Industries

Healthcare & Compliance

Patient data systems, compliance reporting, and workflow automation for regulated environments.

- HIPAA-aware integration pipelines

- Automated compliance dashboards

- Patient workflow digitization

Logistics & Supply Chain

Real-time tracking, route optimization, and inventory visibility across your distribution network.

- ERP/WMS integration

- Automated dispatch workflows

- Supply chain dashboards

SaaS & Tech-enabled

Scale your product infrastructure, integrate third-party tools, and ship features faster with reliable ops.

- API-first architecture

- Multi-tenant infrastructure

- CI/CD and release pipelines

Banking & Financial

Secure transaction processing, regulatory reporting, and customer-facing portals for financial services.

- Regulatory reporting automation

- Secure data integration

- Customer portal modernization

- Case Studies

Featured Case Studies

Browse all case studies →Euro Truck ServiceLogistics firm automated 12 manual workflows in a single 30-day sprint

"Read case study →Ergonnex AI 360Ergonnex AI 360 is a powerful project management platform that helps IT companies manage their projects better with built-in AI-powered analytics

Read case study →PanoramikPanoramic caters to your passion for sharing photos in a social media environment.

Read case study →

Introduction

For several decades, banks operated using legacy core banking systems that were inflexible, batch-oriented, and costly to maintain. These traditional systems, while effective for basic deposits, withdrawals, and account management in their time, lacked the scalability and adaptability.

As digital transformation accelerated across industries, financial institutions began experiencing significant operational constraints with their existing infrastructure.

With the rise of digital banks and tech-driven challengers, the pressure to modernize banking operations became unavoidable. Core banking systems evolved from monolithic architectures into cloud-native, API-first ecosystems to operate and serve customers efficiently.

Understanding The Evolution of Core Banking Systems

A core banking system is the central processing software of a bank. It manages customer accounts, deposits, loans, payments, and transaction posting across branches and digital channels. When integrated well, it lets customers access consistent services from any touchpoint: branch, web, or app.

Early core banking software ran on‑premises, was tightly coupled to proprietary hardware, and depended on legacy programming languages. These systems prioritized ledger integrity and internal control over customer experience. Change cycles were long, and most processing ran in end‑of‑day batches.

Limitations of Traditional Core Banking Technology include:

- Monolithic structures: Difficult to upgrade, scale, or customize.

- Rigid architecture: Inhibits integration with modern APIs or digital channels.

- High operational costs: Requires specialized skills and costly infrastructure.

- Slow product launch cycles: Inflexible systems lead to long development timelines.

- Limited digital capabilities: Not designed for real-time processing or omnichannel delivery.

Did you know? Core banking system was first introduced in the late 1970s to shift from paper-based banking to computerized systems.

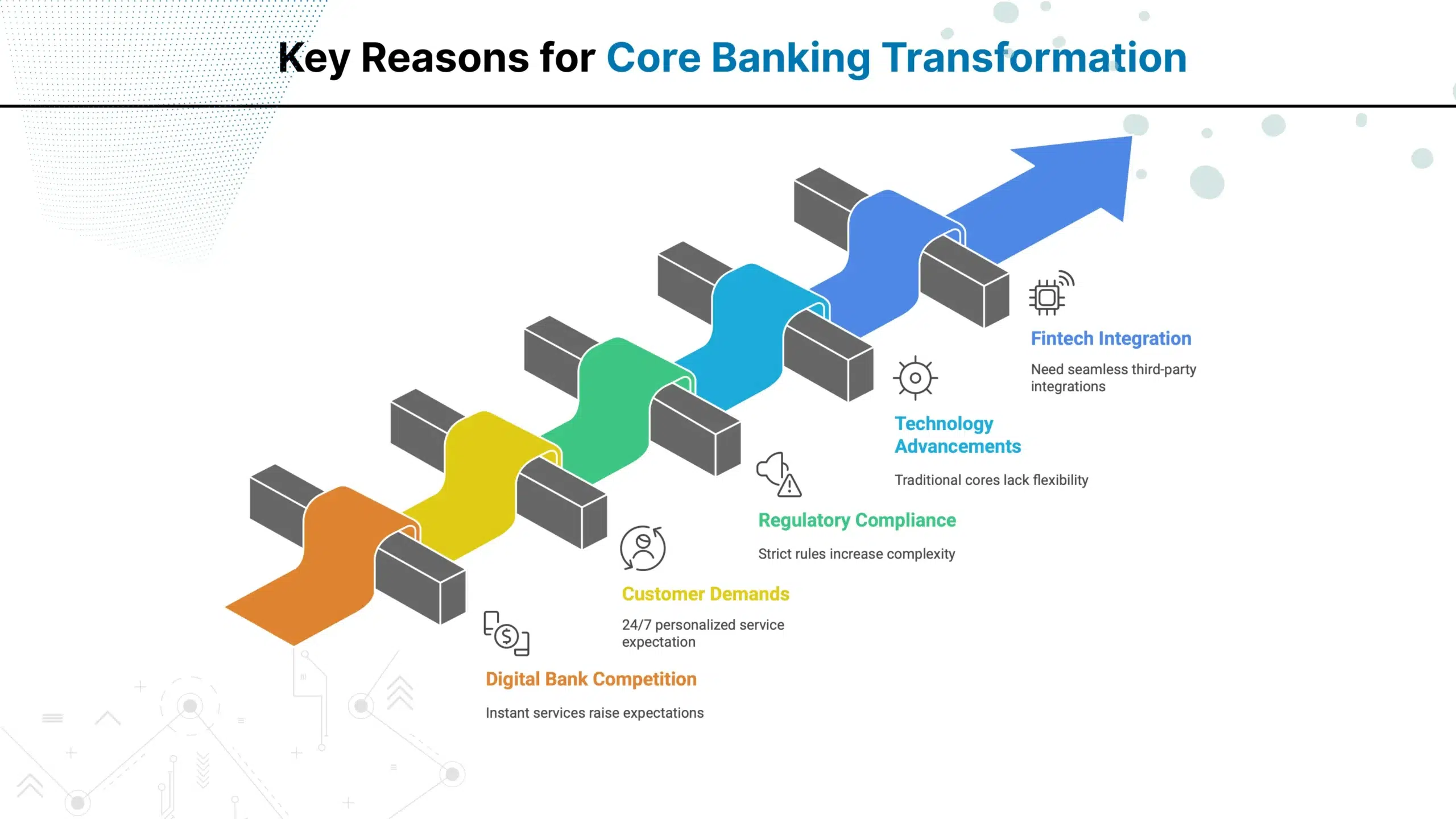

Key Reasons for Core Banking Transformation

Legacy core banking systems were designed to meet the needs of the older era of banking. However, banking evolved, and demand increased for customer-first systems that provide instant services. Here are some main reasons for core banking transformation:

1. Competitive Pressure from Digital Banks

The rise of digital banks and mobile-first platforms introduced seamless and easily accessible services that legacy banking systems could not match. These new entrants offered instant transactions, intuitive interfaces, and zero branch dependency that met customer expectations.

To remain competitive, banks started adopting modern core banking solutions that support modern services.

2. Customer Demand for Always-On Banking Services

Modern customers expect real-time transactions, 24/7 availability, and a personalized experience. Legacy systems, with their batch processing and downtime for updates, cannot deliver this level of availability.

This growing demand forced banks to shift toward digital banking systems that offer continuous uptime, scalable infrastructure, and personalized services to meet customer needs.

3. Regulatory and Compliance Evolution

Global regulators enforced strict regulations around data security, transaction transparency, and reporting timelines. Legacy systems struggle with fragmented data structures, making it difficult to meet these evolving requirements.

Modern core banking transformation strategies integrate automation and other technologies to respond quickly to regulatory changes.

4. Rapid Technological Advancements

The maturity of cloud computing, API-driven ecosystems, and microservices has created an opportunity for banks to modernize their systems. Traditional cores, built as monolithic architectures, lack the flexibility to adopt new technologies.

Banks now leverage core banking technology with modular designs, real-time processing, and cloud-native deployments to deliver faster, more scalable, and future-ready digital services.

5. Fintech Integration and Open Banking Push

Fintechs introduced agile, customer-centric services that banks can no longer afford to ignore. The rise of open banking and API-driven ecosystems forced banks to modernize their infrastructure to enable seamless third-party integrations.

The Role of Technology in the Evolution of Core Banking Systems

Technology has transformed core banking from rigid legacy systems into agile digital platforms. It drives innovation in how banks operate and deliver services. Here’s how this shift reshapes banking:- Legacy Infrastructure Shift: Banks moved core workloads from fixed on‑premises hardware to cloud environments. This change offered flexibility, reduced IT costs, and enabled remote access.

- Transition to Real-Time Transactions: Legacy systems process transactions overnight. Modern systems update data instantly, improving customer experience and reducing delays.

- Introduction of APIs for Integration: Banks built secure API layers that let approved apps and partners plug into core functions. That connection shortens payment steps, speeds loan decisions, and pulls data without manual file transfers.

- Adoption of Modular Architecture: Instead of a single, bulky system, banks now use smaller service blocks. These can be updated individually without disrupting the entire system.

- Use of Automation and AI: Tasks like fraud detection, credit scoring, and issue resolution are now automated. This cuts manual effort, reduces mistakes, and gets answers to customers faster.

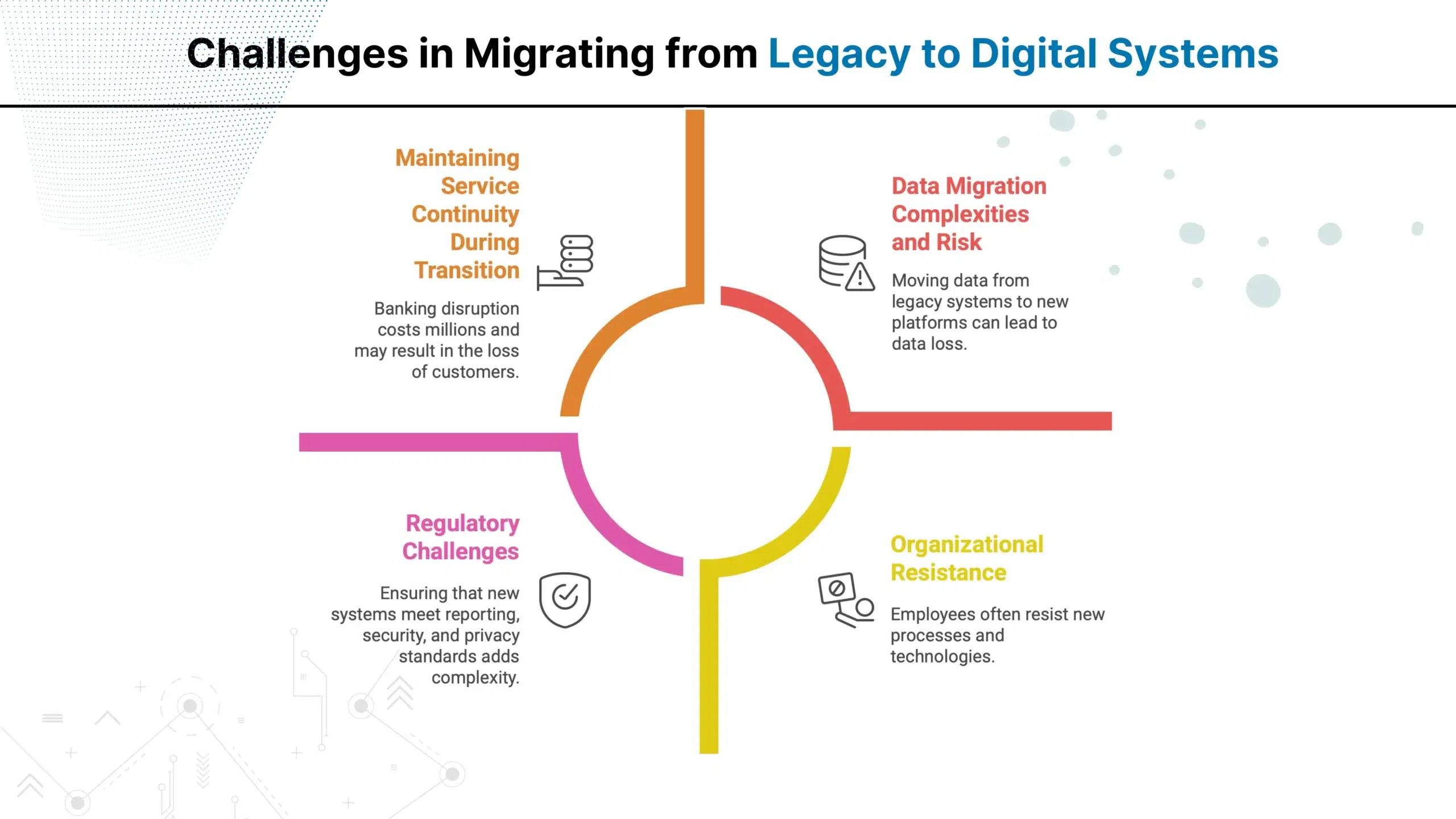

Challenges in Migrating from Legacy to Digital Systems

The migration of core legacy infrastructure to modern digital platforms poses several challenges to financial institutions if not carefully executed.

1. Data Migration Complexities and Risk

Moving decades of customer and transaction data from legacy systems to new platforms can lead to data loss, corruption, or inconsistencies if not handled with precision.2. Maintaining Service Continuity During Transition

Every minute of banking disruption costs millions to banks and may result in the loss of customers. Operations must keep running while upgrading systems.3. Regulatory Challenges

Compliance requirements change over time. Ensuring that new systems meet reporting, security, and privacy standards adds complexity to the migration process.4. Organizational Resistance

Employees often resist new processes and technologies. Training, communication, and leadership support are crucial for the smooth adoption of legacy banking systems replacement.

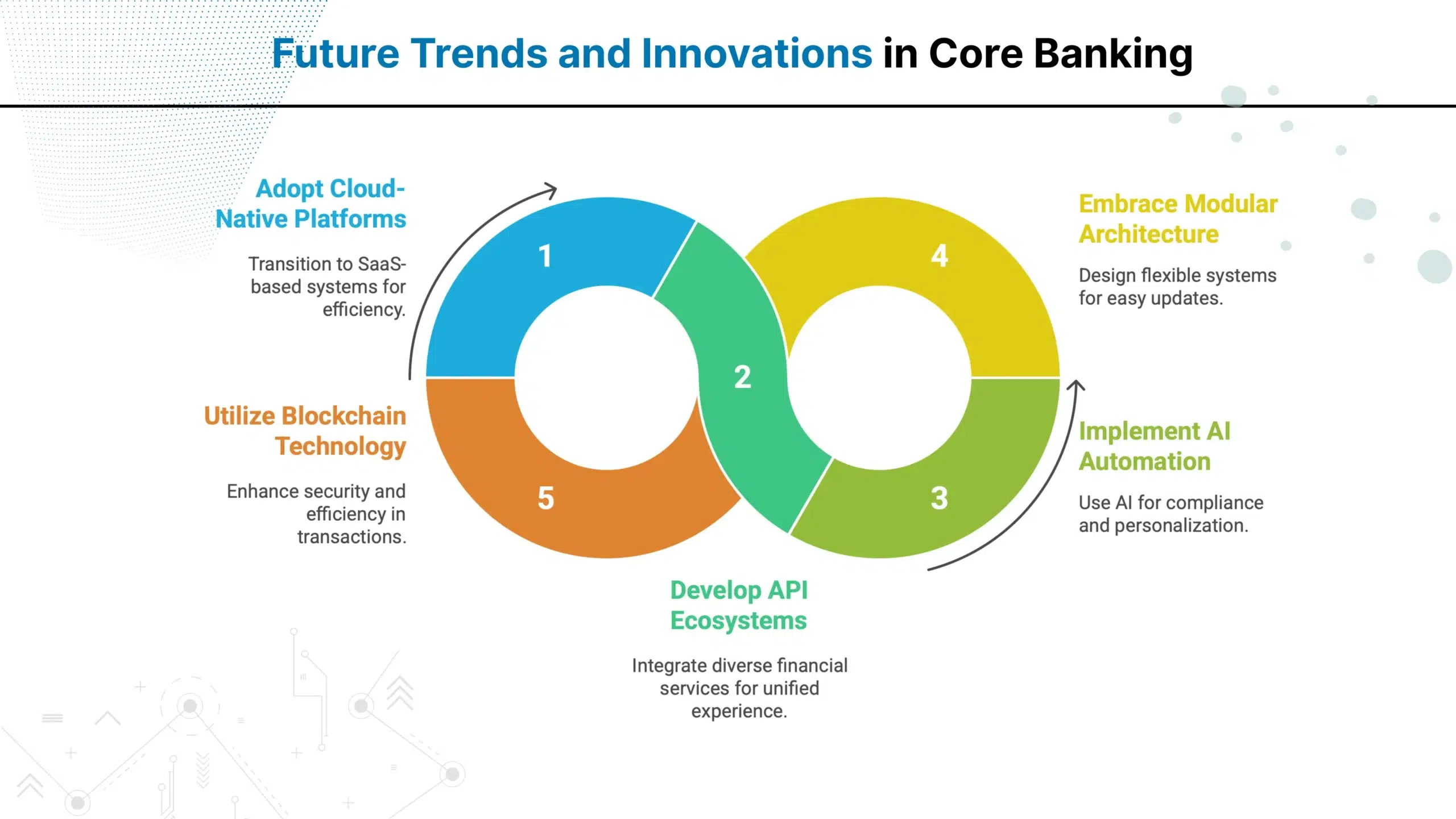

Future Trends and Innovations in Core Banking

The transformation of core banking is accelerating. With advancements in cloud computing and AI, banks are moving beyond traditional systems toward more agile, digital platforms. Here are some future trends in core banking evolution from legacy to digital:

1. Cloud-Native Platforms with SaaS Expansion

Banks are moving from simple cloud migration to full SaaS-based core systems. This approach reduces infrastructure costs, speeds up deployment, and ensures resilience across multiple environments.2. Advanced API Ecosystems and Open Finance

APIs will extend beyond banking into open finance, integrating services like insurance and investments. This creates unified platforms that offer customers a complete financial experience.3. AI for Intelligent Automation

AI in core banking is evolving from analytics to automation. Future systems will use AI to handle compliance checks, fraud detection, and real-time personalization with minimal human intervention.4. Composable and Modular Architecture

Instead of monolithic systems, banks are embracing modular designs. These allow institutions to adopt new features without replacing the entire system, reducing costs and time-to-market.5. Blockchain and Real-Time Settlement

Blockchain will move beyond proofs of concept to handle cross-border payments and real-time settlement at scale. Its transparency and security will improve trust and reduce transaction costs.Conclusion

The shift from legacy cores to digital banking platforms lets banks operate faster and serve customers better. What once took hours or days now happens in seconds with accuracy and consistency. This change is necessary to deal with rising customer expectations, stricter compliance, and advancements in the finance market. As cloud-based systems, AI-powered automation, and modular designs become the norm, banks must modernize their cores to stay competitive.

Do you have more questions?

Have a one on one discussion with our Expert Panel

Every bank today is trying to do more with the same teams. Customer emails are increasing, compliance checks are getting stricter, and service expectations are becoming instant. Yet most internal processes still depend on manual steps. Employees move data from one screen to another, verify documents by hand, and follow long approval chains.

Many enterprise teams treat identity and access as if they are the same thing. They aren’t. Identity confirms who a user is. Access defines what that user is allowed to do. Assuming that an authenticated identity automatically deserves access is one of the most common—and costly organizational security mistakes.

In an era where technology shifts faster than any corporate strategy can keep up, the real concern for IT leaders is how their organization can leverage Microsoft effectively without disrupting operations. This is where the Microsoft Solutions Partner program becomes relevant.

Sahil Kataria

Founder and CEO

Amit Kumar

Chief Sales Officer

QServices Inc. undertakes every project with a high degree of professionalism. Their communication style is unmatched and they are always available to resolve issues or just discuss the project.