-

Industries

Healthcare & Compliance

Patient data systems, compliance reporting, and workflow automation for regulated environments.

- HIPAA-aware integration pipelines

- Automated compliance dashboards

- Patient workflow digitization

Logistics & Supply Chain

Real-time tracking, route optimization, and inventory visibility across your distribution network.

- ERP/WMS integration

- Automated dispatch workflows

- Supply chain dashboards

SaaS & Tech-enabled

Scale your product infrastructure, integrate third-party tools, and ship features faster with reliable ops.

- API-first architecture

- Multi-tenant infrastructure

- CI/CD and release pipelines

Banking & Financial

Secure transaction processing, regulatory reporting, and customer-facing portals for financial services.

- Regulatory reporting automation

- Secure data integration

- Customer portal modernization

- Case Studies

Featured Case Studies

Browse all case studies →Euro Truck ServiceLogistics firm automated 12 manual workflows in a single 30-day sprint

"Read case study →Ergonnex AI 360Ergonnex AI 360 is a powerful project management platform that helps IT companies manage their projects better with built-in AI-powered analytics

Read case study →PanoramikPanoramic caters to your passion for sharing photos in a social media environment.

Read case study →

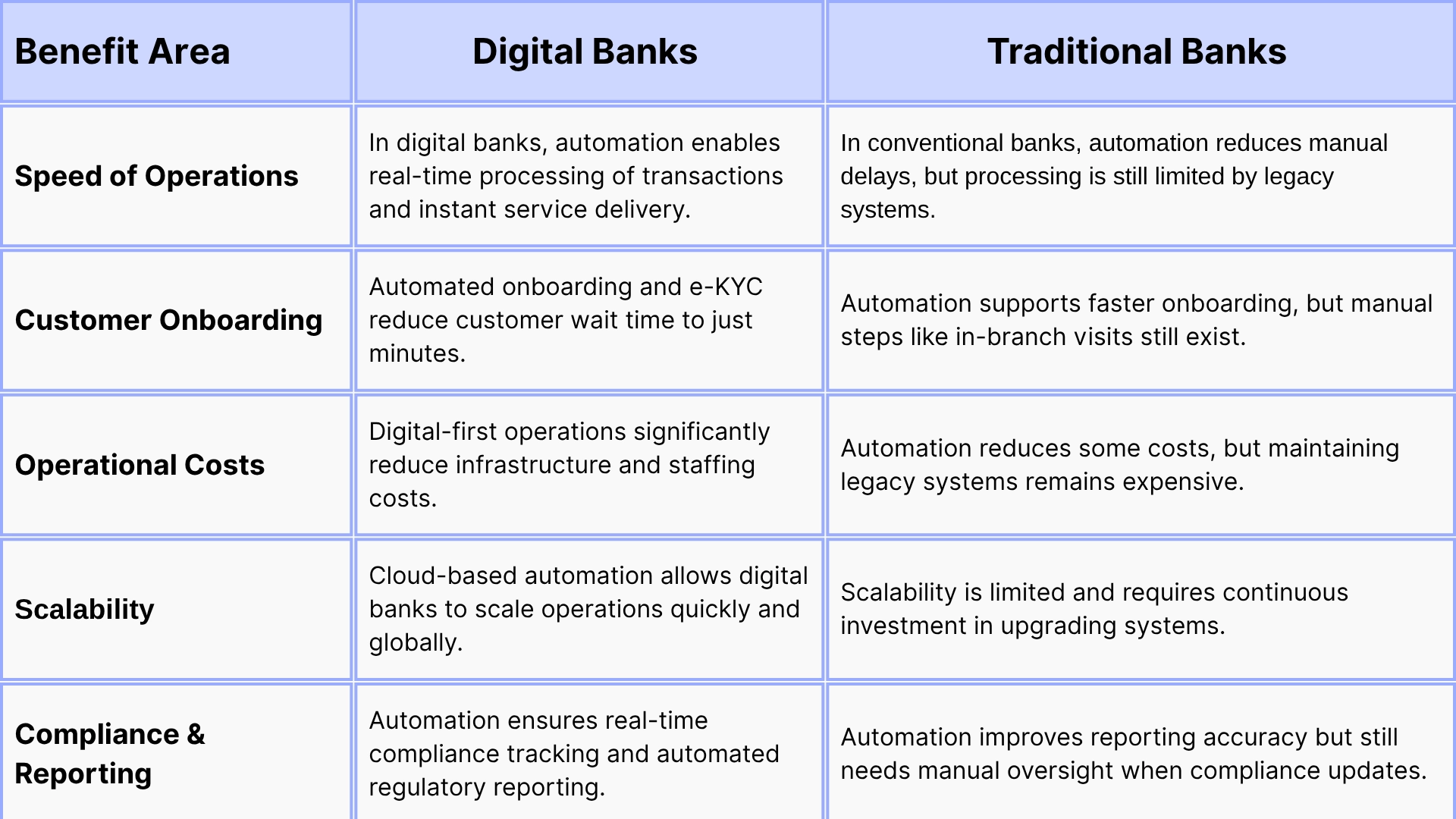

Comparison of Financial Process Automation in Digital vs Traditional Bank

Using automation marks a digital transformation in both banking models; however, its application and impact vary significantly. The table below highlights the differences in automation benefits between digital vs traditional banks.

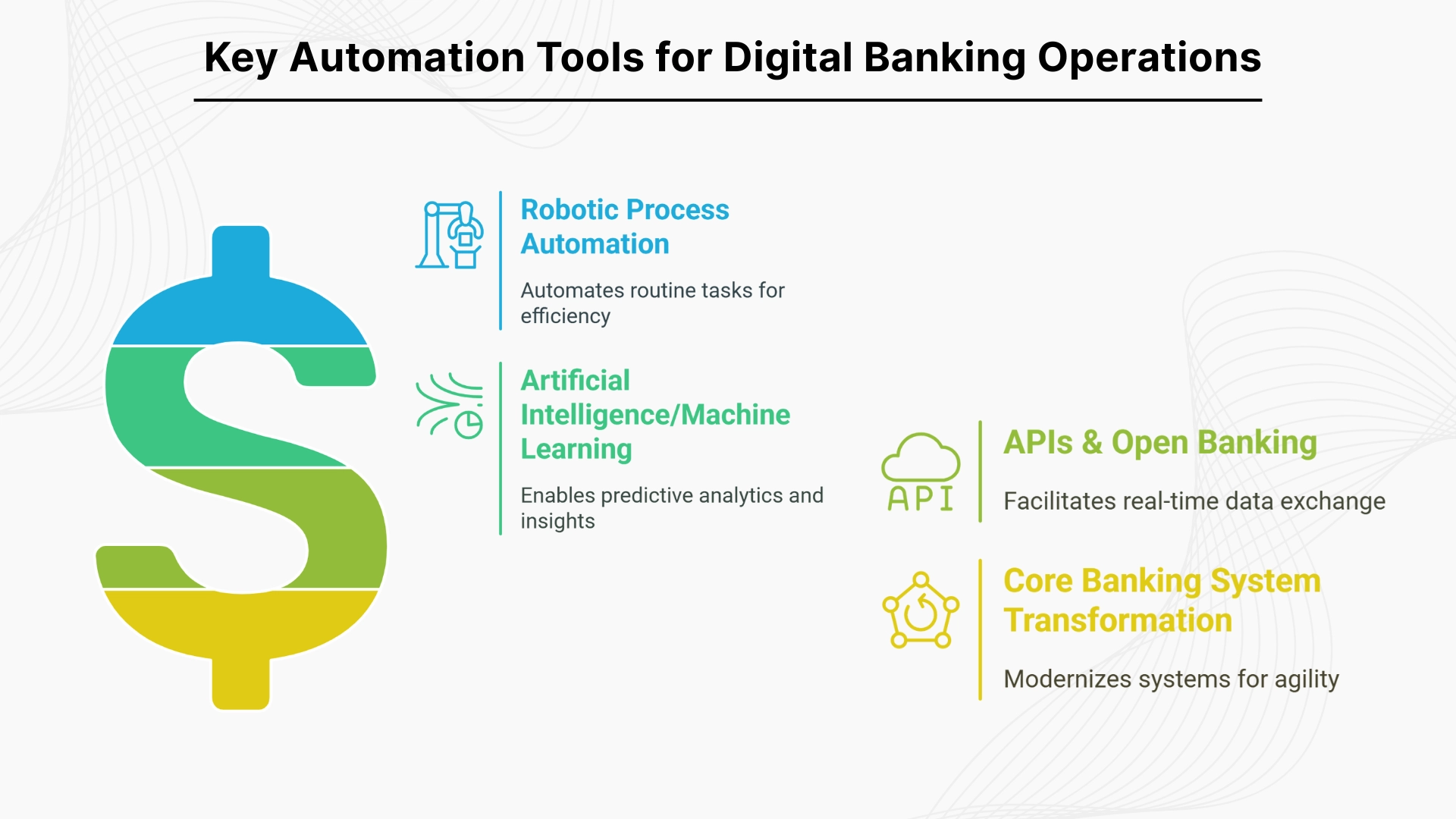

Key Automation Tools for Digital Banking Operations

From credit unions to fintech startups, automation optimizes processes for financial institutions of all sizes. Key technologies that drive digitization in banking operations include:

Robotic Process Automation (RPA)

This technology is known for automating routine task handling that is often repetitive, and rule based. Using Robotic Process Automation (RPA) in banking improves speed and accuracy in document handling, compliance checks, and customer service support.

Artificial Intelligence/Machine Learning

AI-powered automation is used for performing tasks that require human-like intelligence and machine-like workflow. Banks use these technologies to enable predictive analytics and personalized, data-backed insights.

APIs & Open Banking

Integrating APIs into critical areas opens wider opportunities for open banking institutions. It enables real-time data exchange between banks and third-party platforms, allowing secure and fast access to services like payments, account aggregation, and lending tools.

Core Banking System Transformation

Modernizing core systems with cloud infrastructure bring agility to banking operations. They allow easy deployment of automation solutions to handle updates, process data in real-time, and scale services without disruptions.

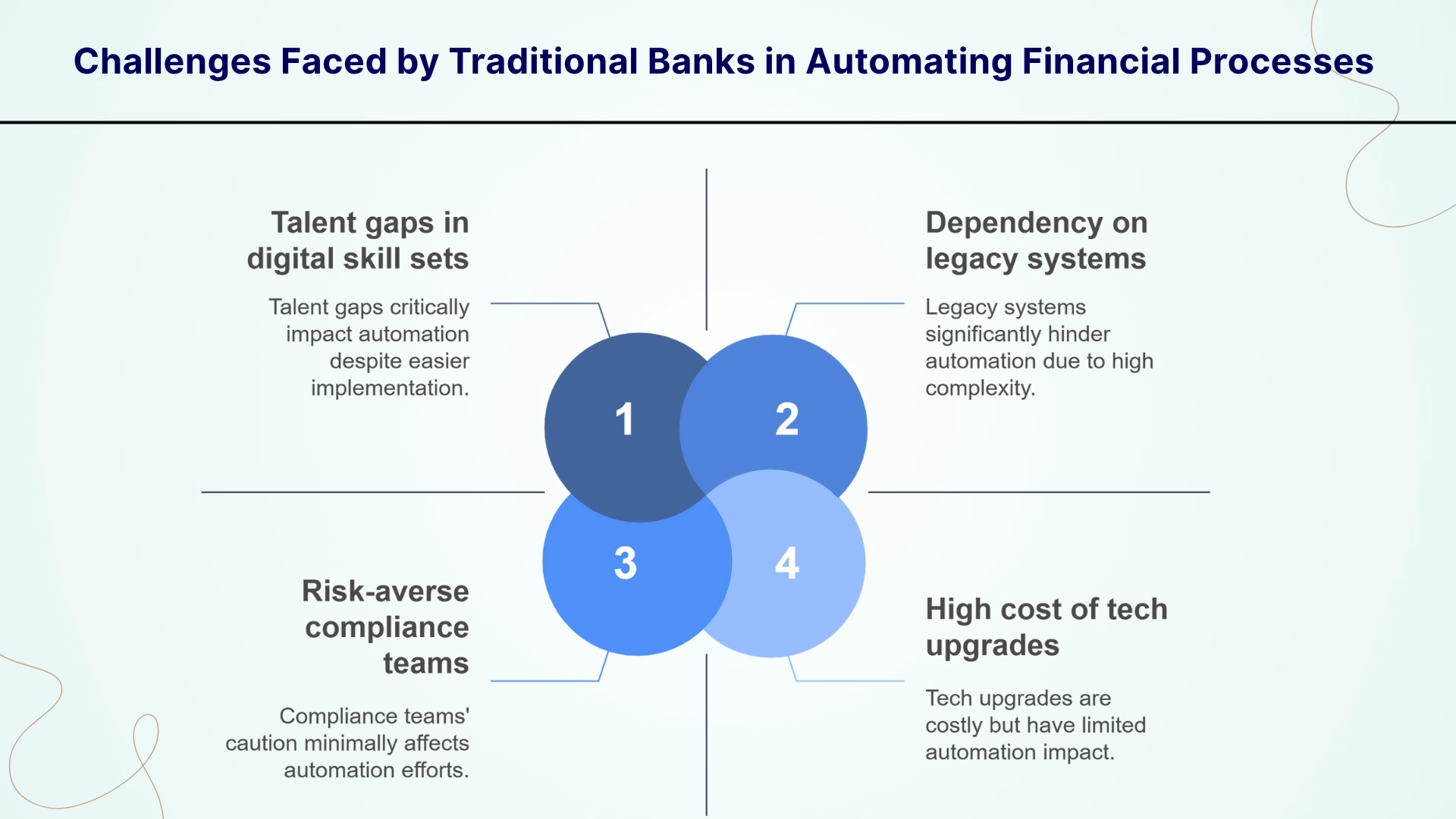

Challenges Faced by Traditional Banks in Automating Financial Processes

Automation eases banking; however, it can be difficult to implement when institutions use outdated systems. Here are some challenges that traditional banks often face with financial process automation.

- Dependency on legacy systems: Many traditional banks still rely on outdated core systems that are not designed for automation. This makes integration slow, complex, and prone to errors.

- Talent gaps in digital skill sets: Banks often face a shortage of staff with the right technical skills. Lack of exposure to automation tools, AI, or cloud systems can lead to ineffective automation efforts.

- Risk-averse compliance teams: Compliance teams in traditional banks are often cautious about new changes. They may delay automation efforts due to concerns around regulatory risks or data handling.

- High cost of tech upgrades: Maintaining legacy systems or bringing new automation tools into older systems can be highly expensive.

Do you have more questions?

Have a one on one discussion with our Expert Panel

Every bank today is trying to do more with the same teams. Customer emails are increasing, compliance checks are getting stricter, and service expectations are becoming instant. Yet most internal processes still depend on manual steps. Employees move data from one screen to another, verify documents by hand, and follow long approval chains.

Secure access is vital for organizations managing digital identities in today’s landscape. While both CIAM and IAM secure user identities, they serve different purposes — CIAM for customers and IAM for employees. This article explores their key differences and how to choose the right system.

For decades, traditional banking systems handled only basic transactions. The digital era exposed their limitations in speed and adaptability. Evolved core banking now powers seamless, future-ready financial services.

Sahil Kataria

Founder and CEO

Amit Kumar

Chief Sales Officer

QServices Inc. undertakes every project with a high degree of professionalism. Their communication style is unmatched and they are always available to resolve issues or just discuss the project.