-

Industries

Healthcare & Compliance

Patient data systems, compliance reporting, and workflow automation for regulated environments.

- HIPAA-aware integration pipelines

- Automated compliance dashboards

- Patient workflow digitization

Logistics & Supply Chain

Real-time tracking, route optimization, and inventory visibility across your distribution network.

- ERP/WMS integration

- Automated dispatch workflows

- Supply chain dashboards

SaaS & Tech-enabled

Scale your product infrastructure, integrate third-party tools, and ship features faster with reliable ops.

- API-first architecture

- Multi-tenant infrastructure

- CI/CD and release pipelines

Banking & Financial

Secure transaction processing, regulatory reporting, and customer-facing portals for financial services.

- Regulatory reporting automation

- Secure data integration

- Customer portal modernization

- Case Studies

Featured Case Studies

Browse all case studies →Euro Truck ServiceLogistics firm automated 12 manual workflows in a single 30-day sprint

"Read case study →Ergonnex AI 360Ergonnex AI 360 is a powerful project management platform that helps IT companies manage their projects better with built-in AI-powered analytics

Read case study →PanoramikPanoramic caters to your passion for sharing photos in a social media environment.

Read case study →

Introduction

Loan processing is a core function of financial institutions. When customers apply for loans, they’re often in urgent need and expect quick decisions. However, banks face delays due to due to manual document verification, credit risk assessments, and compliance checks.

For regional banks and credit unions, the challenge is even greater. With limited staff and infrastructure, staying efficient becomes difficult. They need solutions that handle growing demand with speed and accuracy, which automation does perfectly.

Loan automation systems are redefining the workflow of lending. By speeding up processes, these systems help institutions deliver faster approvals without compromising compliance.

With customer expectations rising, automation has become essential for smaller institutions looking to modernize and scale.

Understanding Loan Process Automation

Loan processing automation means using software to perform regular, rule-based tasks that are involved in the process of lending funds to the customer by a bank.

A loan automation system operates independently across all stages of the loan lifecycle, whether it’s loan application, credit underwriting, or compliance checks. With lending being automated, banks can consistently approve loans faster and with greater accuracy.

What can loan automation software do

A loan automation software in finance can:

Automate loan origination: Digitizes application intake, verification, and initial screening with minimal manual input.

Streamline KYC/AML checks: Integrates regulatory checks through secure APIs and real-time data sources.

Enable automated underwriting: Uses decision models and rules engines to assess creditworthiness.

Manage documentation workflows: Auto-generates, stores, and routes credit and loan documentation securely.

Perform credit checks and scoring: Leverages credit underwriting software for instant credit profiling.

Integrate with core systems: Syncs with platforms like CSI core banking for seamless data flow.

How Automation Streamlines Loan Approvals for Credit Unions and Regional Banks

Small financial institutions like credit unions and regional banks often struggle to process loan applications efficiently due to limited resources. Automation helps them make lending decisions faster as it works as a superficial loan agent for them. Here’s what it enables:

AI-Powered Underwriting for Credit Assessment

Automated systems powered by AI help credit unions and other financial institutions in loan underwriting by providing real-time risk scoring based on behavioural, transactional, and credit data.

Unlike traditional static scorecards, AI-driven underwriting models adapt to trends and anomalies, flagging high-risk applicants proactively.

Automated KYC and AML for Regulatory Compliance

Automation in KYC and AML processes reduces manual errors and ensures compliance with regulatory requirements. With loan automation software, document uploads are automatically classified, verified, and screened against sanctions lists.

Real-Time Insights and Smarter Cross-Sell

Loan automation software provides real-time analytics on loan performance. Credit unions and regional banks can track repayment behaviour, delinquency rates, and product adoption.

This data-driven insight supports smarter decisions and enables timely cross-sell opportunities, such as promoting credit cards, insurance, or investment products based on user behaviour.

Seamless End-to-End Lending Journeys

A fully automated lending system ensures applicants move smoothly from submission to approval and funding. It enables an end-to-end digital lending experience for credit unions as well as regional banks, improving member satisfaction while reducing internal workload.

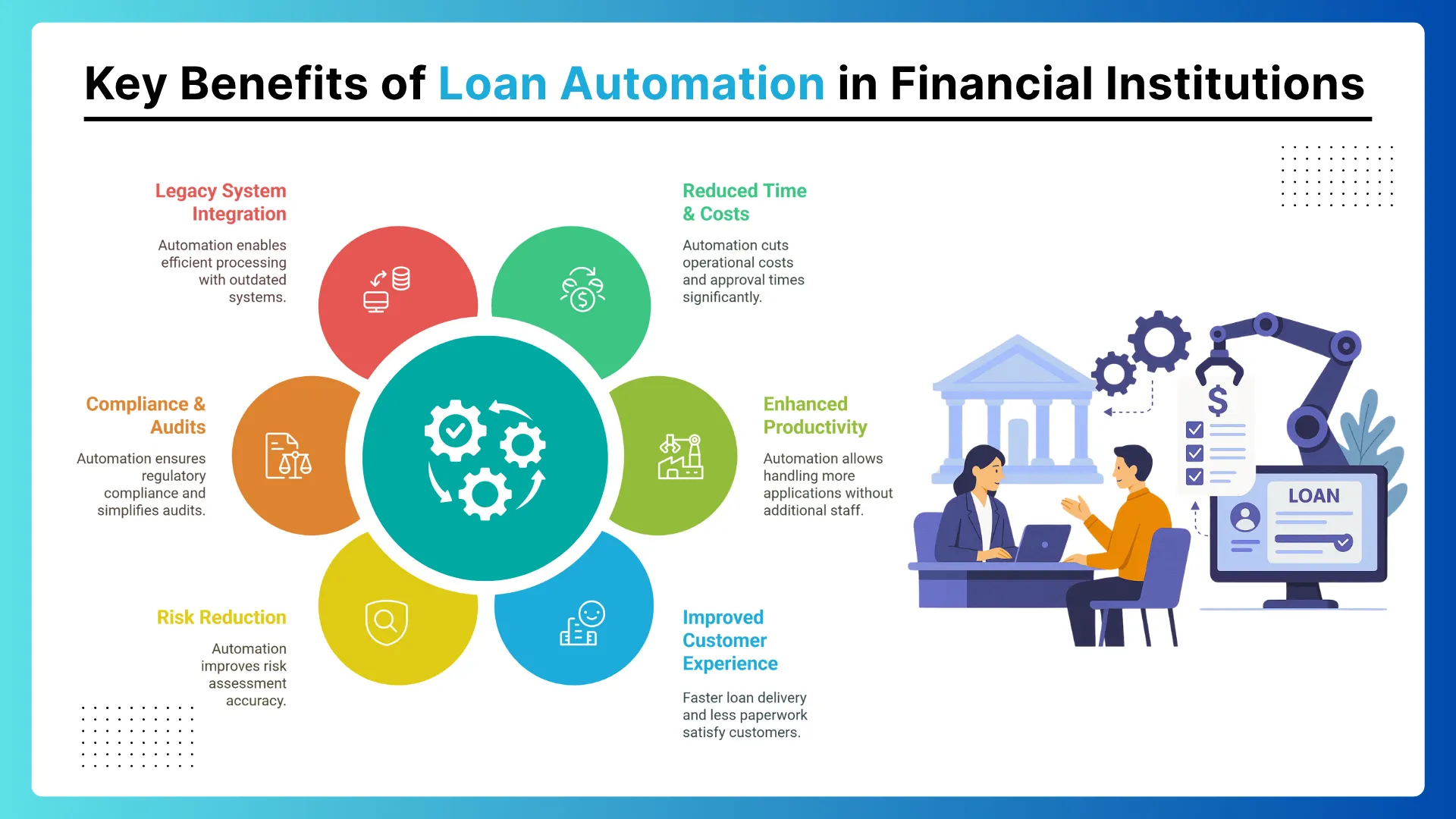

Key Benefits of Loan Automation in Financial Institutions

Automating lending processes optimizes workflows, leading to faster service for customers and greater efficiency for financial institutions. Here are some key advantages of automating credit loan processing:

- Reduced Time, Costs and Errors: By automating data entry, application screening, and initial assessments, banks can save up to 50% on operational costs, drastically reduce human errors and cut approval times by 70%.

- Credit Underwriting Productivity: Automation lets financial institutions handle increased loan applications with greater accuracy without even hiring more underwriters.

- Enhanced Customer Experience: Through fully automated loan software, financial institutions satisfy customers with faster loan delivery and reduced documentation hassle.

- Risk Reduction in Credit Underwriting: Automated underwriting software solutions assess potential credit risks with 40% better accuracy than traditional methods. It does not just rely on credit scores and historical behaviour; it analyses other critical areas as well.

- Improved Audits and Compliance: All actions taken by automated systems are logged and aligned with regulatory frameworks like KYC and AML, ensuring transparency, consistency, and simplified audit preparation.

- Integration with Legacy Core Banking Systems: Even with outdated core banking technology, regional and community banks can enable efficient loan processing by leveraging automation as a service.

Do you have more questions?

Have a one on one discussion with our Expert Panel

Every bank today is trying to do more with the same teams. Customer emails are increasing, compliance checks are getting stricter, and service expectations are becoming instant. Yet most internal processes still depend on manual steps. Employees move data from one screen to another, verify documents by hand, and follow long approval chains.

Secure access is vital for organizations managing digital identities in today’s landscape. While both CIAM and IAM secure user identities, they serve different purposes — CIAM for customers and IAM for employees. This article explores their key differences and how to choose the right system.

For decades, traditional banking systems handled only basic transactions. The digital era exposed their limitations in speed and adaptability. Evolved core banking now powers seamless, future-ready financial services.

Sahil Kataria

Founder and CEO

Amit Kumar

Chief Sales Officer

QServices Inc. undertakes every project with a high degree of professionalism. Their communication style is unmatched and they are always available to resolve issues or just discuss the project.